Alaska's data center opportunity: A reality check and possible next steps

By Peter Asmus, Gwen Holdmann and Erlingur Gudleifsson

February 09, 2024

The role of data centers continues to increase in the lives of ordinary citizens, large corporations and other electricity consumers across the globe. From the surge in interest and application of artificial intelligence (AI) and machine learning (ML) to the more localized needs of remote communities in Alaska, access to the Internet and cloud computing are transforming the economy and the electricity infrastructure that underpins it.

Data Centers come in many forms, designs and sizes. From hyper-scale to edge, the trends in information technology and telecommunications have long been compared to the transformation underway in worldwide power markets (albeit on a slower time scale). According to one estimate, the revenue generated by data center deployments in 2023 could top $325 billion. Of that amount, network infrastructure represents over half of that dollar volume (over $200 billion.) All told, there are 8,000 data centers worldwide that consume roughly 20% of the world’s electricity. Roughly a third of these data centers have been deployed in the U.S.

Alaska has long been seen as an isolated frontier at the top of the world, an outlier in the Arctic with little relevance to the rest of the world when it comes to infrastructure trends, large-scale decarbonization initiatives and growing interest in smaller decentralized electricity networks such as microgrids. This view is no longer valid. Alaska has deployed more microgrids than any other U.S. state, some running almost completely on carbon-free resources. Many of these systems have relied upon older technologies due to the lack of reliable Internet service.

Today, Alaska’s microgrid market is focused on retrofits and upgrades to existing systems. The electric load of Alaska, unlike many other U.S. states, is therefore not on a growth trajectory. A near-term market for smaller, modular but still sustainable data centers is a near-term opportunity being filled by companies such as Greensparc. The firm, for example, is deploying its first modular 100-kW data centers in Cordova, which sits at the mouth of the Copper River, one of the top premier salmon fisheries in the world. There is a clear need to bring similar small-scale data centers under an infrastructure-as-a-service model to these unserved and underserved communities which do not necessarily have the capital to deploy such infrastructure.

Most data centers historically have relied upon armies of diesel generators and lead-acid batteries integrated into UPS systems to provide resiliency. A move toward cleaner assets and microgrids for data centers started about 5 years ago. More recent pressure from the investment community looking toward more nimble decarbonization strategies has the data center industry looking for on-site solutions rather than creative carbon credits from off-site wind and solar farms which served data centers during the transition to a more sustainable pathway forward.

Where are Data Centers Today?

Optimal Power Solutions has deployed thousands of remote off-grid microgrids throughout the Asia Pacific region and most recently in China, Japan and Africa. The company is now part of a new data center initiative called GreenSquareDC and is deploying its first project in Perth, Australia: a 96 MW data center in Australia for Microsoft dubbed “WAi1” to be powered up by a variety of zero carbon technologies that include not only large solar and wind energy assets, but on-site biomass fuels for advanced turbines and green hydrogen fuel cells. The diverse resources would be managed within the context of a large, sophisticated microgrid also supported by dual utility feeds to ensure hyper reliability and resilience.

Would such a large data center make sense in Alaska? One could argue it would because of the following reasons:

- Alaska is strategically located to serve global markets, especially the Asia Pacific region, one of the fastest growing markets for AI/ML and cloud computing in the world.

- Unlike Australia, Alaska has abundant cooling resource possibilities. One of the primary challenges for data centers is cooling loads.

- Data centers would add attractive large commercial electricity loads which could be integrated into the Railbelt grid or be served by stand alone microgrids tapping the full spectrum of renewable resources: wind; hydro; solar; geothermal; biomass; tidal and hydrokinetic.

What are the “ingredients” needed to be a hub for hyper-scale multi-MW data centers?

- Power: Cheap and reliable electricity access and ability to manage a backup generator/battery/microgrid solution for resiliency (see graph below illustrating the relationship between cheap power and data center locations).

- Data Network: Proximity with redundant connectivity pathways (or co-located with) a reliable multi-tenant network peering point that has redundant lines out of it to the Internet. In industry jargon, this is referred to as a gigabit point of presence (GigaPOP)

- Workforce: Local workforce with various technical skills are required to support large-scale data centers. These skills include power and building/cooling management, physical security, and baseline cyber information technology (IT) and operations technology (OT) -- all to manage networking/metering/systems-servers. This doesn't mean local cloud platform engineers are needed. Those sorts of experts can be remote as long as the boots on the ground folks ensure the backbone of data center power plus network plus cooling for the servers is handled and somebody can physically show up and swap out failed components. The people who weave the systems into a platform for other services can be remote.

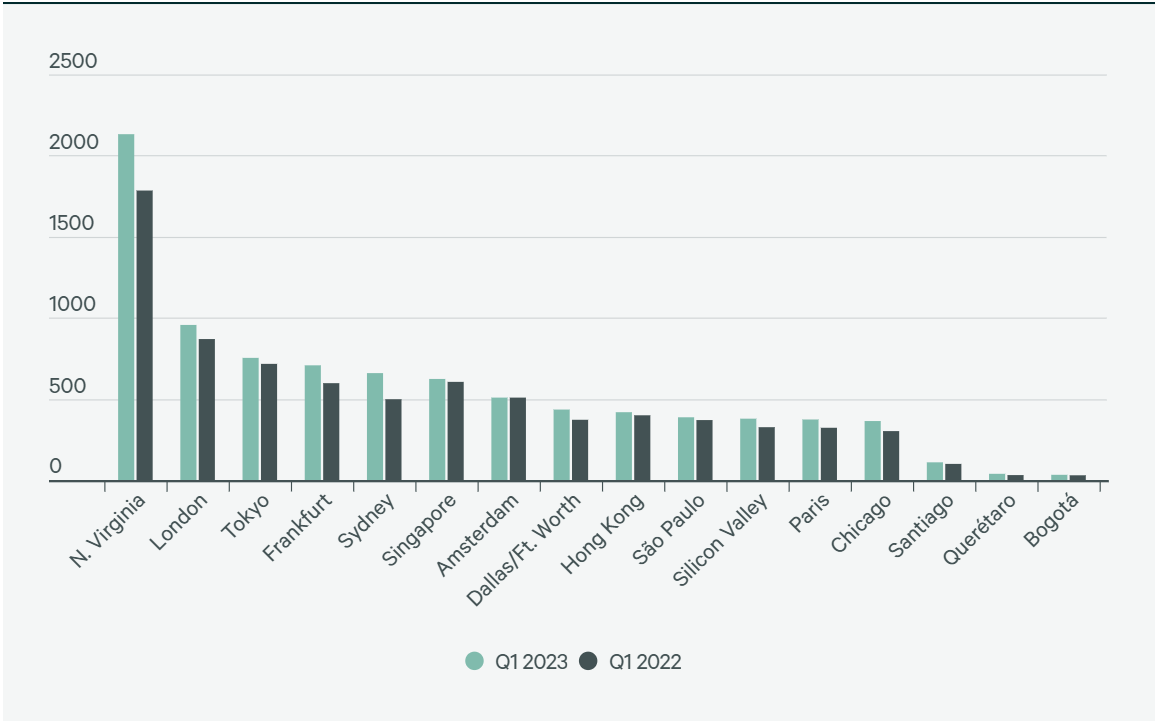

The chart below from a CBRE report on global data center trends shows where the leading regions are for current data center deployments. Note that in the Top 10, four are located in the Asia Pacific region and that a U.S. location - northern Virginia - has a commanding lead in new deployments. The Asia Pacific region is also expected to be fertile ground for microgrids, especially the same kind of off-grid configurations that characterize much of the Alaska market.

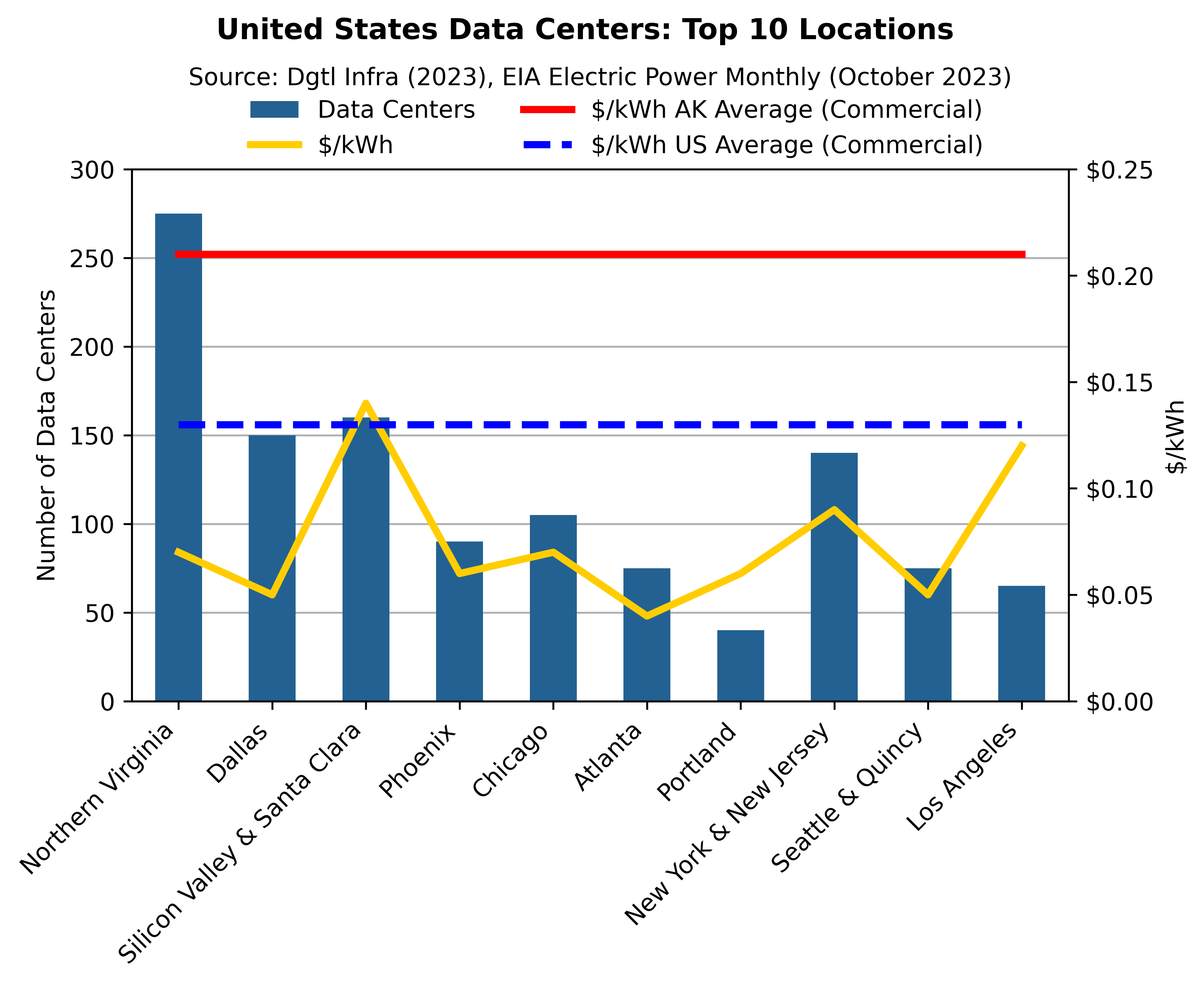

If we zero in on the Top 10 U.S. sites and look at energy costs, it becomes clear these other states hold cost advantages over Alaska. This is a bit of a chicken-and-the-egg situation since large loads integrated into the Railbelt Grid, for example, would reduce overall costs. Yet those loads won’t likely arrive unless electricity costs come down due to economies of scale.

Note that the red line in this graph is the commercial electricity rate in Alaska and is much higher than any other U.S. state. And yet data centers represent the ideal type of customer to build load in Alaska, generating jobs, providing access to underserved communities while also leveraging existing microgrids for vital services. Large-scale data center developments may also offer an alternative to the extractive industries that have dominated Alaska’s economy in the past.

What can Alaska learn from other cold climate sites that have tried to address some of these same issues in attracting new commercial enterprises. Let’s take a look at Iceland.

Data Center Case Study: Iceland

The history of development of data centers in Iceland tracks back to 2007 when Verne Global was established at a former NATO base in Iceland established by Novator Partners and General Catalyst. Verne Global’s operational year wasn’t until 2012.

The first data center in operation (2010) in Iceland was Thor Data Center with an initial installed power capacity of 2 MW provided by the independent power producer sector. Some of the main attractions for the establishment of data centers in Iceland are the accessibility of green energy and cold climate. Thor’s second data center was established in 2014 and had an installed power capacity of 12 MW. It was designed and built to serve the international crypto company Bitfury. Today there are three large data centers in Iceland that are classified as commercial and industrial (C&I) energy intensive users according to Icelandic law (use >80GWh annually at one site or about 10 MW).

The Icelandic data center industry serves three primary markets: The United Kingdom (connections to London and Dublin); Germany (with connections in Frankfurt, Munich and Berlin) and the U.S. (with connections in San Francisco, Seattle, New York, Boston and Washington, DC). In short, 95% of those using the data centers in Iceland are customers located overseas. About 4% of the electricity loads served in Iceland are from the three existing data centers. Energy use by these data centers has increased over time and the job creation benefits have been significant.

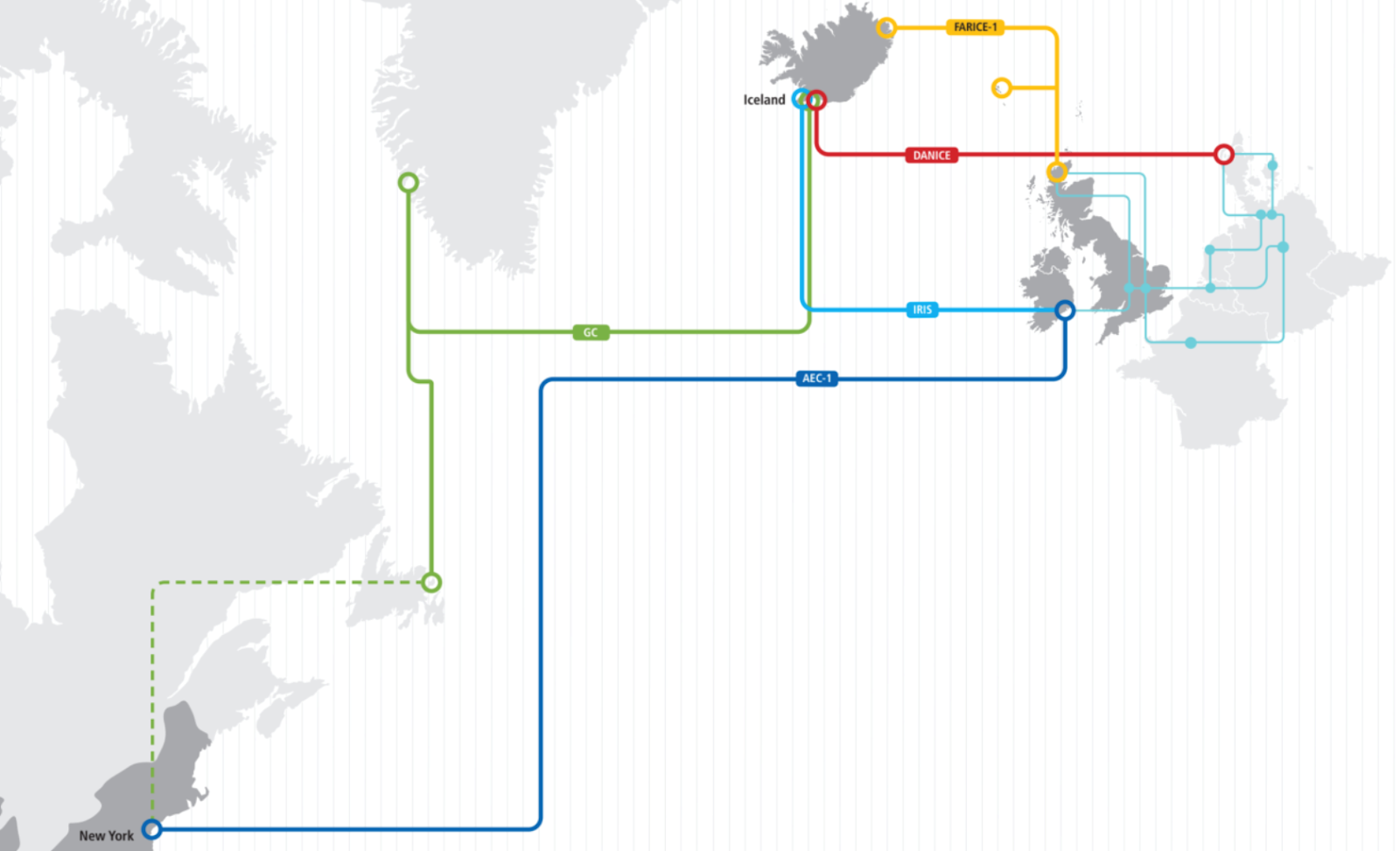

Iceland is connected to both Europe and North America via Greenland and the U.K. (see graphic below). Though Iceland appears to be similarly isolated as Alaska and other Arctic regions, it has been able to take advantage of fiber optic connections to send data to both Europe and the U.S. Alaska, it would seem, could have a similarly sized opportunity to serve the burgeoning Asia Pacific market on the other side of the Pacific Ocean.

What Alaska Needs to Do to Attract Data Center Loads

There are some major obstacles to landing new large electricity loads that could help reduce the cost of electricity in Alaska by increasing economies of scale of new carbon free or low carbon resources. Unlike Iceland, Alaska would need to build out its fiber optic cable lines to access both large opportunities in the U.S. as well as Asia Pacific nation markets such as Japan or South Korea. Among the challenges facing Alaska today are the following:

- Cost of electricity. Alaska’s cost of electricity is among the highest in the U.S., though much lower than some other parts of the world. Hyper-scale data center asset owners typically seek the lowest possible cost for electricity and, most recently, the cleanest sources due to political pressure from environmentalists and the investment community alike to reduce carbon. Other cold climate countries such as Iceland or Greenland have an advantage in this regard, though Alaska has abundant and more diverse renewables that span the full spectrum of available clean energy technologies including tidal and geothermal resources.

- Redundancy for resilience. Many hyper-scale data centers are actually served by two different utilities as a way of ensuring constant 24/7 electricity service. Historically, they’ve also featured armies of diesel generators as back-up sources. A state-of-the-art data center, such as one being developed in Perth, Australia, features dual feeds from a single utility but also is being designed to feature a microgrid without diesel generators. The only part of Alaska that could replicate this model would be on the Railbelt grid, which, unfortunately, is primarily powered by fossil fuels such as Cook Inlet natural gas. New data center loads integrated into the Railbelt could, however, spur efforts to decarbonize this system, which is the primary source of carbon emissions from electricity generation in Alaska.

- Cooling Costs. Data center owners are extremely cost conscious. That's why they are so focused on finding sites with low cost clean power, such as the Google site in Nevada which will run on 100% baseload geothermal energy. Alaska does offer the advantage over a site in western Australia in the sense that abundant cooling resources are available. But cooling costs typically represent 5% or less of ongoing operations and maintenance costs. So perhaps the cold winters may not offer quite as many thermal energy advantages as one would think. Iceland clearly shares this advantage with Alaska.

- Fiber Optic Network Connections. The biggest challenge in siting and building a hyper-scale data center in Alaska revolves around an issue that has little to do with direct costs but instead on infrastructure build-out. While located strategically (theoretically) to serve data hungry Asian Pacific markets, getting data out of Alaska to overseas customers is the challenge. The good news is that there are several projects on the drawing board that would solve this issue, including the three-phase Quintillion fiber optic project. Unlike Iceland or Greenland, which benefit from their vicinity to Europe, Alaska’s remoteness on the data infrastructure front could limit near-term hyper-scale deployments. Or do they?

The harsh Arctic environment poses challenges for installation - and repairs. This past summer, for example, the existing Quintillion line was cut by sea ice scouring operations north of Oliktok Point. Repairs are completed, but this break in the cable caused the loss of internet and cell connectivity for many communities along the Arctic Coast. In the end, the laying of fiber optic cable is the most important factor in Alaska realizing the opportunity to build load and create jobs in the data center space. Luckily, Alaska can help pioneer the small modular systems that have wide ranging applications worldwide for communities without access to any traditional electricity infrastructure in Asia Pacific, Africa and Latin America.

Conclusion: Data Centers To Play a Bigger Role in Alaska?

Despite this and the aforementioned challenges, it is clear the data centers, both small modular edge systems which are predicted to be the faster growing portion of the data center industry in the near-term, and large hyper-scale systems which can increase load and therefore reduce electricity costs for other customers, would make a great fit for Alaska. The former is being pioneered by Cordova with several similarly sized systems to provide data access in remote communities. Look for a forthcoming white paper from the Alaska Microgrid Group offering a playbook for other remote communities in Alaska and throughout the world to learn from Cordova. This is an immediate opportunity to link energy access infrastructure to data access, access that is increasingly important as economic growth becomes tied to having reliable access to the cloud and related services.

Yet if data could be exported outside of Alaska from hyper-scale data centers leveraging low-cost renewables such as hydroelectric or even geothermal, Alaska could attract electricity loads that would lower costs and tap local expertise on how to design and build resilient systems that meet the demand for sustainable energy solutions that is building up across the globe. Right now, this opportunity is a long-term bet, but one that could pay dividends as Alaska seeks to leverage its geographical location. Rather than being an isolated spot at the top of the world, Alaska could be a strategic data exchange hub to serve some of the fastest growing economies in the world.