Managing Your Award - Financial

Charging of Administrative and Clerical Salaries and Certain Other General Administrative Expenses to Federal Funds

Background:

Under federal regulations and sponsor requirements, general administrative expenses including but not limited to administrative or clerical salaries, office supplies, postage, local telephone costs, photocopy costs, network charges, telecom infrastructure and, cell phones, etc. should normally be treated as a F&A cost and recovered through the F&A cost rate (also known as indirect cost rate).

In exceptional circumstances where the nature of the work performed requires extensive departmental support (defined as an unlike circumstance) the F&A type cost may be treated as a direct charge. However, costs such as administrative or clerical salaries and other general administrative costs must directly benefit and be easily identified with the particular sponsored project.

Principal Investigators and department administrators must ensure that the direct charging of F&A type costs must comply with sponsor requirements, University policy, and the applicable cost principles, 2 CFR Part 200.

Administrative/Clerical Staff Expenses:

This guidance is issued to define the appropriate charging of administrative or clerical salaries and other general administrative expenses consistent with 2 CFR Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

The direct charging of administrative or clerical salaries may be appropriate where the nature of the work performed under a particular project requires an extensive amount of administrative or clerical support which is significantly greater than the routine level of such services provided by the academic department.

Examples of circumstances where the direct charging of salaries of administrative or clerical staff and other department expenses may be appropriate are as follows:

- Large complex programs, such as Program Projects, environmental research centers, engineering research centers, and other grants and contracts that entail assembling and managing teams of investigators from a number of institutions.

- Projects which involve extensive data accumulation, analysis and entry, surveying, tabulation, cataloging, searching literature, and reporting (such as epidemiological studies, clinical trials, and retrospective clinical records studies).

- Projects that require making travel and meeting arrangements for large numbers of participants, such as conferences and seminars.

- Projects whose principal focus is the preparation and production of manuals and large reports, books and monographs (excluding routine progress and technical reports).

- Projects that are geographically inaccessible to normal departmental administrative services, such as research vessels, radio astronomy projects, and other research field sites that are remote from campus.

- Individual projects requiring project-specific database management; individualized graphics or manuscript preparation; human or animal protocols; and multiple project-related investigator coordination and communications.

The examples above are illustrative of the same criteria that are applied to the treatment of items such as office supplies, postage, local telephone costs, photocopying, network charges, cell phones, etc. Direct charging of such expenses may be justifiable when the expenses are related specifically to the technical substance of a project or there is an unusually high level of expense because of the nature of the activity.

Conditions Under Which Administrative or Clerical Salaries May be Charged Directly:

The charging of administrative or clerical salaries may be appropriate ONLY IF ALL of the following conditions are met:

- Administrative or clerical services areintegralto the particular project; meaning the services are essential to the project’s goals and objectives;

- Individuals involved can be specifically identified with the particular project;

- Such costs are explicitly included in the budget or have the prior written approval of the Federal awarding agency; and

- The costs are not also recovered as indirect costs.

Care should be exercised to ensure costs incurred for the same purpose in like circumstances are treated consistently as either a direct or F&A cost. For example, salaries of technical staff, laboratory supplies, animals, animal care costs, travel costs, and specialized service center costs should be treated as direct costs whenever identifiable to a particular cost objective. Other general administrative items such as office supplies, postage, and memberships should normally be treated as F&A costs unless:

- The expenses are essential, vital, or fundamental to the project’s goals and objectives; and

- Such costs are explicitly included in the budget and budget justification or if required by the sponsor’s terms and conditions, received prior approval of the sponsor.

F&A type costs not requiring the prior approval of the sponsor must be documented. The Principal Investigator and the unit should have the documentation retained in the department’s file for audit purposes.

Additional information can be found in the University of Alaska Accounting and Administrative Manual: Section 100: D-05 Accounting for Administrative or Clerical Services on Sponsored Projects

Billing & Invoices

UAF collects money from federal and nonfederal sponsors using one of three methods:

- Drawing from an established line of credit (LOC draw)

- Submitting an invoice

- Advances and scheduled payments

The type of billing is established based on the sponsor requirements documented in the award terms and conditions. Regardless of the billing type, OGCA is responsible for the billing for all sponsored projects.

On a monthly basis, the PI and unit business offices with delegation authority should review their accounts through Banner and Q-menu to:

- Ensure that financial information accurately reflects the organization’s activity.

- Identify possible inaccuracies through a comparison of actual expenditures with the approved budget.

- Verify payments have been received from the sponsor.

Budget Revisions

During the life of a project, it may become necessary to modify certain aspects of the original project. Such changes may involve re-budgeting of funds among expense classes or adjusting the length of a project period. In order to minimize the administrative burden associated with revised budget requests, many sponsors allow some flexibility to adapt award spending patterns to match the changing circumstances of the sponsored project. The AwaRe form is used for generating a request to the sponsor. Any questions regarding re-budgeting requests and compliance with sponsor terms and conditions should be directed to OGCA.

In general, a formal revised budget approval request to the sponsor is required in the following circumstances:

- Budget revision restrictions are imposed in the terms and conditions: These restrictions may range from a prior approval requirement for any budget revisions to a requirement for line-item or total budget revisions up to a certain threshold (e.g., re-budgeting flexibility up to 10% within proposed line items).

- Budget revisions are due to a significant change in the scope of work (SOW): SOW changes may require a considerable amount of funds to be shifted between expense categories. However, even if significant changes are not anticipated, all re-budgeting requests based on a change in the SOW must be submitted and approved by the sponsor.

Budget revisions to reflect new financial realities, such as salary increases, new employees on the project, adjusted fringe benefit rates, etc., generally do not require sponsor approval. However, PIs should contact OGCA for guidance and/or clarification of budget revision requirements.

Carryover Expenses

While many sponsors allow awardees to carry forward unspent funds from one budget period to the next, certain award types have restrictions on carryover and require prior approval before such unspent funds may be used. Your Notice of Award (NOA) will indicate if approval for carryover of funds between budget periods is required. Please note that subawards are also impacted by carryover requirements. Please contact OGCA for assistance.

NOTE ON SPONSOR APPROVAL

In cases where sponsor approval is required, OGCA will restrict the affected funds while approval is being sought, coordinate the request for approval with the department and the sponsor, and if approval is granted, authorize the continued use of the funds.

Cash Management

As part of financial administration activities, OGCA manages the cash-related activities of UAF’s sponsored projects. Essential responsibilities include:

- Process Letter-of-Credit (LOC) cash draws and web-based invoicing for Federal awards.

- Prepare and file the quarterly Federal Financial Report (FFR) for the LOC awards, and perform funding, cash and expenditure reconciliations.

- Process installment or cost reimbursement invoices for Non-Federal or Federal Pass-Through grants and contracts and act as the point of contact for billing inquiries.

- Process receipts of sponsor payments and ensure they are credited to the correct award and invoice.

- Track sponsored project receivables and initiate collection communication.

- Reconcile sponsored project receivable and follow up on unbillable issues.

The goal is to maintain appropriate levels of cash flow for UAF’s sponsored projects while ensuring financial compliance with Federal regulations, sponsor requirements, and University policies.

Billing and Payments

- In general, sponsored-award invoices are generated on a monthly basis. For billing inquiries, please email uaf-gcbilling@alaska.edu

- For payments to the University via check, please read the information below for deposit instructions.

- For payments to the University via wire transfer, please uaf-gcbilling@alaska.edu for bank information.

- UAF University’s Employee Identification Number is: 92-6000147.

Payment Deposit Instructions

- If sponsor payments are received by any University department for sponsored awards, please note the UAF’s Banner G# on the check stub and hand-deliver the payment and any accompanying documents to the following location for deposit:

- 2145 North Tanana Loop

West Ridge Research Building (WRRB) Suite 008

PO Box 757880,

Fairbanks, AK 99775-7880

Please do not forward check(s) via campus mail.

Cost Allocation

Allocation is the process of assigning a cost, or a group of costs, to one or more projects. If a cost benefits two or more projects, the cost must be allocated to (i.e. shared between) the projects based on the proportional benefit to each project. If the exact proportions cannot be reasonably determined because of the interrelationship of the work involved, then the costs may be allocated using one of the cost allocation methodologies described below. (§200.405(d)).

The basis for the allocation methodology chosen should be documented at the time the cost is incurred. The allocation should also be approved in advance by the Principal Investigator (PI) of the projects to which the costs are allocated. When it is not possible to allocate costs to the benefiting sponsored projects at the time when the goods or services are purchased, costs must be recorded in a non-sponsored account instead of being charged to a sponsored project (§200.405(c)). The redistribution of these costs to a sponsored project is a cost transfer.

Allocable Costs (§200.405(a))

Allocation Methodologies

Different allocation methodologies may be required for different types of expenses. The basis for the allocation methodology chosen should be part of the auditable documentation retained for the project.

Allocation based on FTEs

Acetone purchased for use in a laboratory is needed for the technicians working concurrently on Projects A, B, and C in the amount of $500/month. There is one technician working on Project A, two working on Project B, and three working on Project C. The expense allocated to Project A is $83/month (1 technician / 6 total technicians x $500/month). The expense allocated to Project B is $167/month (2 technicians / 6 total technicians x $500/month). The expense allocated to Project C is $250/month (3 technicians / 6 total technicians x $500/month).

Allocation based on usage

The monthly cost of supplies/expendables to maintain a lab computer system is $1,000. The computer system is solely used for Projects A and B. The computer operating system keeps a log of users and their time on the system. A reasonable base to allocate the expense would be computer user hours. Project A assistants have 100 combined user hours a month and Project B assistants have 80 combined user hours a month. The expense allocated to project A is $560 (100 user hrs / 180 total user hrs x $1,000). The expense to Project B would be $440 (80 user hrs / 180 total user hrs x $1,000).

Allocation based on effort

A research assistant spends 80% effort on Project A and 20% effort on Project B. The research assistant uses supplies totaling $3,000/month on the two projects. Usage is directly related to the amount of effort devoted to each project. Therefore, $2,400 (80% of $3,000) is charged to Project A and $600 (20% of $3,000) is charged to Project B.

Additional examples of methodologies that may be used as a basis for allocating costs:

- Number of experiments: The cost of syringes is allocated based upon the number of experiments performed on each project.

- Sampling: Cost of laboratory supplies is allocated based on actual usage records for a representative sample.

- Number of patients served: The cost of tests is allocated based upon the number of patients served by each project.

- Square footage: The cost of glassware for the two laboratories that are conducting similar research is allocated based upon the square footage of the two laboratories.

Unacceptable Allocation Methodologies

Administrative expenses may not be distributed or rotated among sponsored projects. Pooled allocation methodologies may not be used to charge administrative costs to sponsored projects except by service centers with approved rates.

Costs may not be allocated based on:

- Amount of available funds on a given award

- Budgetary convenience (e.g. to accommodate an award that is either over or under budget, budget is ending soon, etc.)

- Offset (i.e. costs charged to budget A one time and budget B the next time)

- Rotation of charges among sponsored projects by month without establishing that the rotation schedule credibly reflects the relative benefit to each sponsored project

- The budgeted amount in the contrast rather than the actual usage

- Assigning charges to a sponsored project in advance of the time the actual expense is incurred

- Exclusively charging to sponsored projects when the expense also supports non-sponsored activities

- Avoidance of restrictions imposed by regulations or terms of a given award

Documentation

Allocation methodologies must be documented and auditable (§200.405(d)). Documentation should include the costs to be allocated and the basis for the methodology applied. The Uniform Guidance, specifically 2 CFR 200.333, governs record retention under federal grants. The Federal Acquisition Regulation, specifically FAR 52.215-2, governs record retention under federal contracts. The University of Alaska UA Office of Records and Information Management has additional information on record retention: Retention and Disposition Schedules

If an allocation is applied across multiple accounts, this backup documentation should be retained.

Allocation Methodology Best Practices

- Document the allocation methodology prior to, or contemporaneously with, the costs being incurred and allocated.

- Document why the specific methodology was chosen; show how the methodology relates to the costs being allocated and the benefit received by the awards.

- Retain the supporting documentation in the department (in accordance with the University’s Records Retention Policy) so it is available for review and audit.

- Review allocation methodologies periodically to ensure they are reasonable.

- Methodologies based on sampling, surveys, etc. should be reviewed and updated at least once each fiscal year. Significant changes made to the population may signal the need to review the allocation methodology.

Effort Certification

As a recipient of federal funding, UAF is required to comply with the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (“Uniform Guidance”), as well as other federal requirements for certifying effort expended on sponsored awards. UAF requires all individuals who receive federal sponsored funding to comply with University policies and sponsoring agency regulations regarding the proposing, charging, and reporting of effort on those awards.

UAF receives significant funding for sponsored projects from federal and state governments, private foundations, organizations, and industry. There must be accurate effort planning and confirmation when these funds are expended for salaries and wages.

Uniform Guidance (2 CFR 200.430 – Compensation-personal services.) outlines the requirements for non-Federal entities to track and report payroll-related costs on Federal awards, usually referred to as “effort reporting” or “effort certification”. The primary requirement is that strong internal controls must exist for the reporting of salaries and wages to ensure that the charges “are accurate, allowable, and properly allocated” to the correct award. The reported effort must also be “be incorporated into the official records of the non-Federal entity,” which UAF handles via OnBase.

UAF faculty and staff are expected to charge their time to sponsored awards commensurate with the committed effort expended on all activities they perform. Payroll charges to sponsored awards and cost sharing recorded for faculty and staff serve as the initial data points for the University’s effort reporting system.

UAF’s practice is to utilize an after-the-fact effort reporting system to certify that salary either charged or cost shared to sponsored awards is reasonable and consistent with the work performed. The individual’s effort is first assigned to specific awards in the payroll system based on anticipated activities. Actual effort expended on each project is certified by a responsible person with suitable means of verification that the work was performed, generally the principal investigator, at the end of specified reporting periods. The effort certification should be a reasonable estimate of how time was expended. Uniform Guidance Section 200.430(c) states:

“It is recognized that teaching, research, service, and administration are often inextricably intermingled in an academic setting. When recording salaries and wages charged to Federal awards for IHEs [institutes of higher, a precise assessment of factors that contribute to costs is therefore not always feasible, nor is it expected.”

Additional background information is available in Statewide's Accounting and Administrative Manual, Section D-04.

All individuals involved with the administration and conduct of federally-sponsored award activities, including central and departmental sponsored project administrators, principal investigators, and other research personnel must comply with this policy.

Adherence to this policy is required for all effort related to federally-sponsored awards as well as any non-federal awards where the non-federal sponsor requires effort reporting.

- Non-Exempt Employees: certify every 2 weeks via their submitted timesheets

- Exempt Employees: certify with trimester Effort Certification Statements.

Principal Investigators (PI)/Faculty Members:

- Understand their own as well as their staff members’ (non-faculty personnel) levels of effort committed, charged and reported on all applicable awards.

- Review, initiate corrections if necessary, and electronically certify their individual their Trimester Project Effort Certification(s).

- Communicate significant effort changes to the department business administrators.

- If applicable, the PI must formally request via the OGCA Effort Certification email (uaf-ecert@alaska.edu) that the certification responsibility be delegated to another individual who has sufficient technical knowledge and/or is in a position that provides for suitable means of verification that the work was performed.

- Review salary charges on awards on a monthly basis with grant manager and identify any effort-related changes and communicate with administrators to post corrections, if needed.

- Re-certify and electronically sign if effort changes are made after a statement has been certified.

Department/Unit Business offices:

- Monitor and review effort commitments, salary charges, and cost sharing on all applicable awards.

- Communicate to OGCA any changes that require sponsor notification and/or approval.

- Review salary charges with PI/faculty member and post any salary distribution updates and/or corrections in a timely manner.

- Check effort certifications for accuracy during the review period.

Office of Grants and Contracts Administration (OGCA):

- Communicate significant changes in effort to sponsors.

- Maintain UAF’s effort reporting policy and procedures.

- Provide effort reporting training, guidance on requirements, and oversee University-wide compliance with UAF’s Effort Reporting Policy.

- Manage the business/functional aspects of the electronic effort reporting system through OnBaseManage data uploads into OnBase.

- Staff the effort certification help email and respond to functional questions and issues.

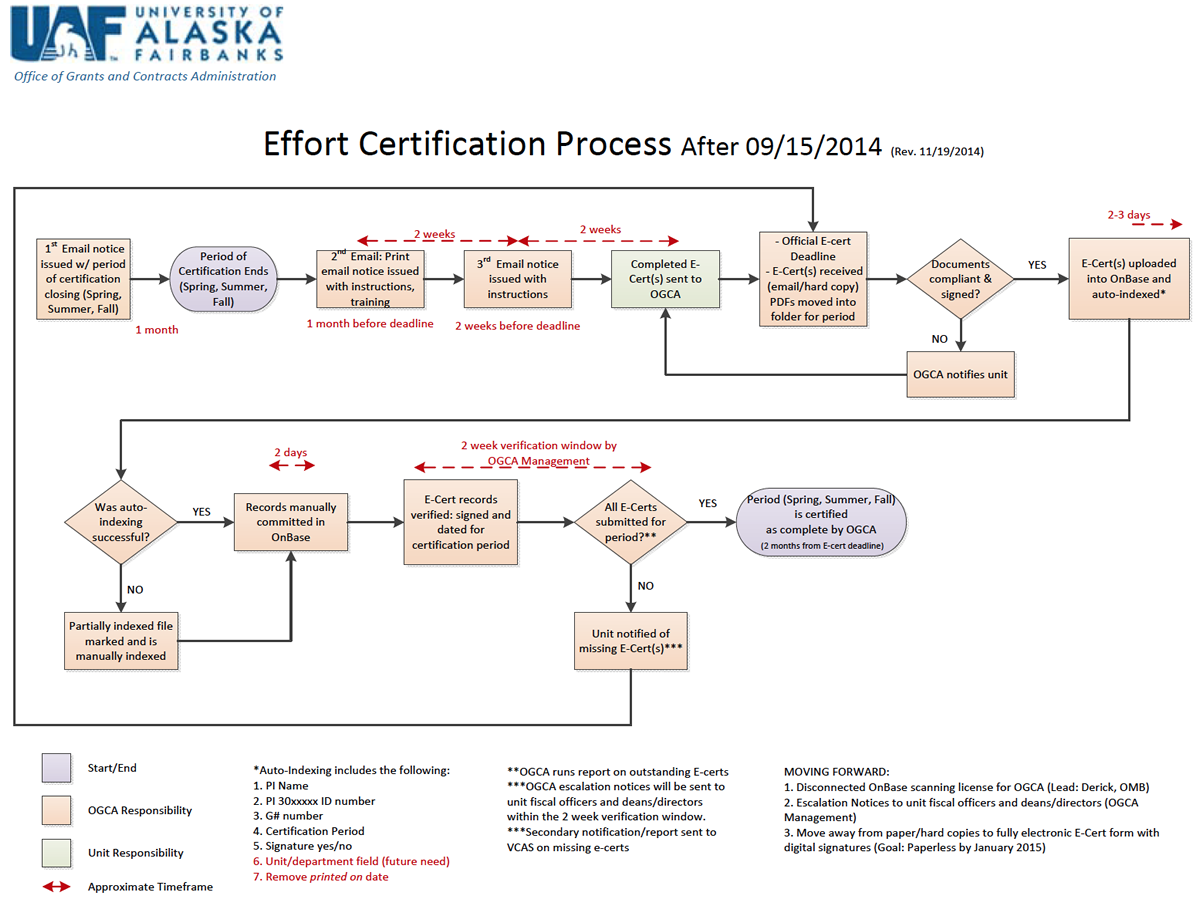

Reporting and Certification Process

- There are three effort reporting periods at UAF each fiscal year (trimester basis): (1) fall, (2) spring, and (3) summer.

- Once the effort reporting period has ended (one month before the certification deadline), OGCA will send out an email with approval to print out and complete needed effort certifications, instructions on completing the certifications, and information regarding available training.

- During the month window, from the end of the reporting period up to the certification deadline, OGCA receives the completed effort certifications via email (uaf-ecert@alaska.edu) and complies them electronically. The certifications are verified for completeness, compliance, and signatures.

- Fully complete, compliant, and signed certifications are batch uploaded into OnBase for auto-indexing. If auto-indexing is successful, the record can then be committed in OnBase. If auto-indexing fails, then the record must be manually indexed and committed in OnBase.

- Once the records are committed in OnBase, OGCA initiates a two-week verification phase, checking that all certifications are signed and dated within the appropriate reporting period and that a unit has submitted all required certifications. If a unit has any missing certifications, OGCA will send requests on a regular basis until all required certifications are received, indexed, and verified.

- Once all certifications have been received, indexed, and verified, OGCA will certify the effort reporting period as complete. This entire process is completed within 60 days from the certification deadline.

Note that total effort on Effort Certification Statements must equal 100% and cannot exceed 100%.

Spring 2025 (R3 - R10)

- Time: Jan 12, 2025 - May 3, 2025

- Print : May 19, 2025

- Due: June 16, 2025

Summer 2025 (Run 11 - Run 17)

- Time: May 4, 2025 - Aug 9, 2025

- Print: Aug 18, 2025

- Due: Sept 22, 2025

Fall 2025 (R18 - R2)

-

Time: Aug 10, 2025 - Jan 10, 2026Print: Jan 19, 2026Due: Feb 23, 2026

Spring 2026 (R3 - R10)

- Time: Jan 11, 2026 - May 2, 2026

- Print: May 18, 2026

- Due: June 22, 2026

Entertainment and Meeting Costs Using Sponsored Project Funds

Under the guidelines imposed by the Uniform Guidance, entertainment costs are considered unallowable direct charges, except where specific costs that might otherwise be considered entertainment have a programmatic purpose and are authorized either in the approved budget for the Federal award or with prior written approval of the Federal awarding agency.

Entertainment costs are defined in the U.S. Office of Management and Budget’s Uniform Guidance, 2 CFR 200.438 as:

Costs of entertainment, including amusement, diversion, and social activities and any costs directly associated with such costs (such as tickets to shows or sports events, meals, lodging, rentals, transportation, and gratuities).

Section 2 CFR 200.403(c) of the Uniform Guidance requires that we apply our policies and procedures uniformly to both federally-financed and other activities of the university. Therefore, UAF’s related procedural statements are also applicable to non-Federal awards. The basic criteria for charging entertainment costs are similar for non-Federal sponsored projects, but it is also important to be familiar with the particular requirements or restrictions of each non-Federal sponsor. When allowed by the non-Federal sponsor, a written justification for the inclusion of entertainment costs should be provided in order to explain why these are necessary to fulfill the research objective of the project, and to ensure that the cost directly benefits the project being charged, even when the non-Federal sponsor may follow more flexible spending guidelines. If funds are being used through the UA Foundation there may be exceptions.

Examples of Entertainment and Meals Situation

The following are examples of common situations that arise on sponsored research awards. These examples are intended as a guideline for determining the classification and allowability of expenses. We realize that the guidelines are subject to interpretation on a case-by-case basis. Please contact OGCA for questions regarding a specific case.

- The institution invites a renowned scientist to deliver a paper directly related to a sponsored research award. The Department of Biology provides coffee and cookies during a break before a related question and answer session. The cost of the refreshments are not entertainment and should be allowable on a sponsored research award, so long as they are reasonable. They are associated with a meeting where the predominant purpose is the delivery of information regarding a related sponsored research award.

- After the meeting, the dean of the School holds a reception for the scientist where beer, wine and hors d'oeuvres are served. These costs are considered entertainment and generally unallowable on sponsored research award.

- Instead, the dean takes the scientist and his department chair out for dinner. Alcohol is served. This is also considered entertainment, and is not generally allowable on a sponsored research award.

- The College puts this scientist up at a local inn after the talk. The costs of subsistence would be allowable on a sponsored research award where the principal purpose of the meeting like this, was dissemination of technical information.

- The Physics Department receives a sponsored research award to hold a symposium for leading scientists to discuss a new particle. In its sponsored research proposal, the Department listed the activities it planned to conduct, and the sponsored research proposal specifically provided for a working dinner the night before. This would be allowable on the sponsored research award since there was such a specific provision. If alcohol is served it would not be allowed.

- From time to time, the Chemistry Department Chairman holds lunches for the members of her Department at Wood Center to discuss academic and research issues. Unless the primary purpose of the lunch is dissemination of technical information, as evidenced by a formal agenda, the sponsor would probably contend that the primary purpose was the meal, not the discussion (which could presumably have been held without the expenses); so the cost of lunch would be considered entertainment and generally not be allowed on a sponsored research award.

- The provost travels to Washington to recruit a department chair. The reasonable cost of travel and subsistence (less alcohol, of course) would not be considered entertainment. Presumably this would include the costs of lunch or dinner with the recruit, assuming that it was inappropriate to meet at the recruit's place of business. Similarly, the reasonable cost of the recruit's travel to your institution would not be considered entertainment

- The Dean holds a reception in honor of a department’s 25th anniversary. This is entertainment. Presumably the exclusion would also run to any glossy publications that were produced on or after the affair.

Meetings and conferences may be allowable, if the primary purpose is the dissemination of technical information and is necessary and reasonable for successful performance. Costs that may be allowable include rental of facilities, speakers' fees, costs of meals and refreshments, local transportation, and other items incidental to such conferences unless further restricted by the terms and conditions of the award 2 CFR 200.432.

Sponsored funds are not to be used for meals or coffee breaks for intramural meetings of the University or any of its components, including, but not limited to, laboratories, departments, and centers.

Auditors and agency regulations are applying a conservative interpretation of the cost principles in this area. Therefore, the University requires that meeting and conference expenses directly charged to a sponsored project be supported by documentation showing that the activity is directly related to the project. Examples of acceptable documentation include:

- A line item in the approved project budget for the meeting or conference

- Narrative in the proposal referring to the meeting or conference

- A published agenda for the meeting or conference

- Correspondence with the sponsor

Federal Financial Reports (FFRs)

Description:

A Federal Financial Report (FFR) is required for recipients of federal funds to report the status of funds for grants or assistance agreements. A FFR is a statement of expenditures sent to the sponsor of a grant or contract.

FFRs are prepared and submitted by Office of Grants and Contracts Administration (OGCA) on behalf of the Principal Investigator (PI)/UAF. Sponsor guidelines specify the level of detail on a financial report.

Major Elements:

The format of the FFR report is specified by the sponsor and includes the following major elements:

- Identification: grant number, sponsoring agency, project title and funding period.

- Report Period: period over which the spending occurred.

- Summary of transactions:

- Letters of credit (cash is received via daily electronic transfers for most federally sponsored projects);

- Cost reimbursement payments (payments made by check or wire transfer in response to invoices sent by OGCA) or;

- Advance/scheduled payments (payments made by check or wire transfer in advance of the start date or on a schedule specified in the award documents).

- Expenditures are all allowable costs not reported as obligations that are incurred during the budget period.

- Facilities & Administrative (F&A) costs (also known as indirect costs) are costs applied to the grant at a percentage rate approved by the federal government The facilities and administrative cost rate, total charges, and base upon which they are charged are detailed on the FFR.

- Obligations are funds set aside to pay for commitments incurred within the budget period but which have not been paid prior to the preparation of the FFR.

- Program Income is income earned as a result of the sponsored activity. Program income must be approved by the sponsor, or allowable according to the sponsor's terms and conditions, and must be reported on the FFR.

- Cost-Sharing Contributions are costs that contribute to a project but which are provided by other non-federal sources. Mandatory and Committed cost-sharing must be documented and met before the FFR can be submitted.

- Unobligated Balance consists of awarded funds remaining after all expenditures and obligations have been reported. Disposition of unobligated funds is specified in the sponsor regulations.

- Cash Receipts come from the following sources:

- letters of credit (cash is received via daily electronic transfers for most federally sponsored projects);

- cost reimbursement payments (payments made by check or wire transfer in response to invoices sent by OGCA) or;

- advance/scheduled payments (payments made by check or wire transfer in advance of the start date or on a schedule specified in the award documents).

- Certification: name, title and contact information of authorized institutional official, date

- Additional details: sponsor driven

Common formats for the FFR are specified by the sponsor and are prepared by OGCA including:

- SF 425 – Federal Financial Report

- SF 269 - Financial Status Report

- SF 270 - Request for Advance or Reimbursement

- SF 272 - Federal Cash Transaction Report

- Some sponsors often have unique format and/or site requirements. Sponsors post FFR reporting information and requirements on their website.

Grants Management Forms from the US Office of Management and Budget Available now through Grants.gov

Non-Federal Sponsors specify financial reporting requirements and often provide a form for the report.

Submission:

The FFR is reported to the awarding agency either in paper form, or electronically by entering the data into the agency’s web-based forms, in accordance with the awarding agency’s instructions.

Frequency and Types (sponsor driven):

- Interim

An interim FFR is a financial report that covers a period within a longer budget period (i.e., monthly, quarterly, or semi-annually). - Quarterly

A quarterly FFR is a financial report that covers a 3 month period. Report can be calendar quarters or budget quarters based on the project start date. - Annual

An annual FFR is a financial report that typically covers a one-year period. Report can be calendar based or project based on the project start date. - Final

A final FFR is a financial report that is prepared at the end of a project.

Due Dates:

The schedule for submitting required financial reports is generally specified in the award documents of a grant or contract.

FFRs may be due at the end of the Budget Period, Project Period and/or award period normally due within 90 days after the expiration date, and may be required at interim times as well.

Financial Reporting

The goal of the financial reporting as a function of OGCA is to provide Principal Investigators and department/unit business office administrators with quality support services and financial compliance guidance along with effective stewardship of sponsored awards.

Most sponsors require financial reporting to determine the use of sponsored funds on either a monthly, quarterly, annual or other reporting basis. The OGCA’s main responsibility is to ensure that the deadlines for financial reporting are met and that we are in compliance with the federal, state, sponsor specific and/or UA/UAF’s policies and procedures depending on the type of award. UAF shall submit timely financial reports to the sponsors of research and other scholarly activity that:

- Accurately reflect the actual use of sponsored funds as recorded in the financial records of the University

- Ensure that all reports are in compliance with the sponsor’s terms and conditions

OGCA can provide guidance and assistance as well as answer any questions that may arise on a day to day basis.

At the conclusion of the award, after the financial report is filed with the sponsor, and all financial obligations are satisfied, OGCA is responsible for closing the award within the University’s financial system.

Match/Cost Sharing Commitment vs. Match/Cost Sharing Certification

Cost sharing also known as matching is the portion of the project expense borne by the university and not by the sponsoring agency. It includes all contributions, including cash and in-kind, that a recipient makes to an award. Shared costs are typically paid from departmental or discretionary funds or provided by a third party.

Cost sharing disclosed to the sponsor in the proposal constitutes a promise that university funding will be provided to directly support the project. Once an award is made, the cost sharing documented in the proposal becomes a binding commitment.

Pre-award: (Match/Sharing Commitment)

The PI prepares a cost share pledge by:

- Clearly documenting cost sharing in the proposal budget justification.

- Omitting from the proposal text any normal university resources necessary for the project which are not offered as voluntary committed cost sharing. If deemed necessary, this type of information should be narrative in nature and must not include quantifiable financial information.

- Obtaining signed documentation from each funding source that has promised to contribute. Letters of funding commitment from third parties must be on the contributor’s letterhead.

- If the contribution is from the university, a signed letter from the chancellor, provost, dean/director or the authorized official’s signature is acceptable.

- Submitting all signed documentation with the proposal package to OGCA

Post-award: (Match/Sharing Certification)

- Department administrators are responsible for recording and tracking cost share expenses. The PI is responsible for ensuring that all cost share contributions are captured correctly and that cost sharing obligations are met in a timely manner.

The PI and/or the department administrator must finalize and approve cost share contribution reports (certification) so that OGCA can submit the cost share data to the sponsor in accordance with the reporting terms defined in the award agreement. A commitment letter is not a certification.

Certification of cost sharing/match documents that what was proposed actually happened and that the third party has provided what they indicated they would in their commitment letter.

Third Party Cost/Match Certification Template

Office of Finance & Accounting (OFA) - UA Match Funds

Posting Transactions to Sponsored Accounts

The spending of any funds awarded by the federal government to University of Alaska Fairbanks (UAF) is governed by the “Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; Final Rule” (Uniform Guidance), published by the Office of Management and Budget (OMB).

In addition to the Uniform Guidance, UAF must comply with the Cost Accounting Standards (CAS) located at 48 CFR 9905.501, 9905.502, 9905.505, and 9905.506. The purpose of the CAS is to ensure consistency in:

- Estimating, accumulating and reporting costs (CAS 501)

- Allocating costs incurred for the same purpose in like circumstances (CAS 502)

- Accounting for unallowable costs (CAS 505)

- Cost accounting periods (CAS 506)

Additional information regarding CAS Exemptions can be found at CAS Exemptions

Pre-Award Spending Advance Approval (PASAA)

(under Award Negotiation – PASAA)

This process provides a mechanism to allow Principal Investigators (PIs) to incur costs for sponsored research awards that have not yet been awarded to the University, or for incremental awards for which the new budget period has not yet been awarded to the University, all in cases where there is a high likelihood that the awards will be received.

Pre-Award Spending

Pre-Award Spending is spending that occurs on an award before the funder’s official award notice is received by the University. Pre-award spending may also include spending that occurs after the official receipt of the award but before the account has been established for the award.

Advance Accounts

Advance Accounts are accounts from which spending occurs on an award (a) before the funder’s official award notice is received by the University or (b) before official notification that the renewal or continuation of an existing award has been approved, obligated and authorized, provided reasonable assurance by the sponsor.

OGCA will approve Advance Accounts and authorize Pre-Award Spending when the following conditions are met:

- A funder (e.g., federal or state agency, private foundation) has provided sufficient documented written assurance from an appropriate organizational official, as determined by OGCA, that funding is imminent.

- The PI can demonstrate a need to incur expenses prior to the official start date of the award

(i.e., pre-award spending if permitted) or prior to the receipt of the fully executed award document (i.e., advance accounts). Situations in which an account may be requested for a new project include, but are not limited to, the following: the purchase of equipment or supplies to conduct a project or the bulk purchase of materials to secure a time-limited discount. On continuing projects, advance spending may be requested to purchase supplies or to support critical employment commitments. In the case of contracts being negotiated, pre-award spending may be approved where there is a high degree of likelihood that the contract terms and conditions will be resolved and are in accordance with regular university contract parameters.

- A full copy of the funding proposal for the project is on file within OGCA.

- All required research assurances and compliance approvals have been obtained, e.g., for

Conflict of Interest, IRB, IACUC, IBC, Environmental Health and Safety (EH&S) and Risk

Management.

- The proposed dates for the advance account are no more than 90 days prior to the anticipated start of the award. Pre-award spending will occur within the 90-day period prior to the start date identified by the sponsor.

The maximum duration of advance accounts is 90 days. The value of advance accounts is capped at 25% of the total value of the award from the sponsor.

Responsibilities

Principal Investigators (PIs) are responsible for the content of pre-award or advance account requests submitted to OGCA for review and approval, e.g., that requests are congruent with approved institutional policy and sponsor requirements. Pre-award or advance account should be sent to OGCA.

OGCA will be responsible for the assignment of the grant number and for ongoing review of account status.

Financial Risk

If the award to the University does not occur or the project dates are inconsistent with the account set-up dates, the financial risk is assumed by the PI’s academic unit. The department/ unit will be required to provide a general account number when the risk account is established to ensure that all unauthorized or unfunded pre-award expenses are subsequently allocated to the department/ unit.

Prior Approval Requests

What Are Prior Approval Requests?

- For changes related to an award certain sponsors may require prior approval in the form of a formal request.

- Examples of Prior Approval Requests are No Cost Time Extensions, Carry Forward, Re-budgeting, Changes in the Scope-of-Work or PI, and Pre-Award Spending.

- Some Prior Approval requests can be completed and approved internally under Federal Demonstration Partnership (FDP) regulations.

Why Are Prior Approval Requests Important?

- The Terms and Conditions set forth in the agreement determine the parameters in which changes can be made.

- Failure to acknowledge these parameters and obtain these approvals may result in penalties such as termination of funding by the agency or disallowance of expenses.

Prior Approval Request for Grants and Cooperative Agreements

Prior Approval Request for Grants and Cooperative Agreements: Request for Approval of Administrative Action Under Federal-wide Standard Research Terms and Conditions (RTC)

- All requested actions must include a scientific justification. Most actions require additional information to be submitted.

- The information below provides general guidance on additional information required.

- Before submitting any administrative request, refer to agency-specific terms and conditions and prior-approval matrix, at: National Science Foundation.

- If further information is needed, contact OGCA assigned to your department/unit.

- Change in PI or Other Key Personnel

Additional information to be submitted includes but not be limited to:- Name of new/interim PI

- Current and pending support or other support (PHS) for new/interim PI

- Biographical sketch information for new/interim PI

- Significant Reduction in Effort

Most sponsors allow rebudgeting without prior approval under RTC unless there is a change in the scope of work.

Additional information required:- Amount of funds to be rebudgeted and to/from which categories

- Impact on affected budget categories

- Assurance that request will not change existing total cost commitment for current and future budget periods

- Establish a consortium or transfer substantive programmatic work to a third party

(NOTE:Not required for awards under FDP or expanded authorities unless action represents a change in scope.)

Additional information required:- Effect on budget

- Any changes in scope of work

- Assurance that request will not change existing total cost commitment for current and future budget periods

- Signed Subrecipient Commitment Form

- Statement of work for subrecipient

- Budget and justification for subrecipient

- No-Cost Time Extensions (NCE)

The fact that funds remain at the expiration of the grant is not, in itself, sufficient justification for a no-cost extension.- First Time Requests:

Requests for first time no-cost time extensions under Research Terms and Conditions (RTC) or expanded authorities must be submitted within sufficient time for OCGA to notify the awarding agency of the extension at least 10 DAYS PRIOR to the expiration date of the project period. (Note: some sponsors require more than 10 days, please refer to the link above for agency-specific requirements). - Additional Requests:

Extensions beyond the first no-cost extension require approval from the sponsor. Submission times vary. Refer to agency specific requirements.

Additional information required (for any request for NCE):- Scientific justification including progress to date

- Length of extension requested

- Amount of and reason for unobligated balance

- Plan for use of funds during extension period. (Include categorical budget detail, in text format, of requested direct and F&A costs.)

- Conflict of interest disclosure(s)

- Animal and/or human subject use:

- If yes, provide approvals

- If no, state in justification

- First Time Requests:

Other information as required by sponsor

- Carryover Requests

(NOTE:Unless restricted on the terms of the award, this action is generally allowable under FDP or expanded authorities for certain federal awards.)

Additional information required:- Differs greatly among sponsors; refer to agency-specific terms and conditions.

- Significant Rebudgeting Requests

(NOTE:For awards issued under FDP or expanded authority, this action is necessary only when rebudgeting represents a change in scope. SNAP awards are required to include this action as part of the noncompeting award process.

Additional information required

- Amount of funds to be rebudgeted

- Which budget categories funds will be moved from and to

- Implications on F&A costs

- Indicate whether there will be a change in scope

- Assurance that request will not change existing total cost commitment for current and future budget periods

Request to Carryover Unobligated Funds

Request sent to OGCA using the Award Request (AwaRe) Form. The process is facilitated by OGCA to the agency/sponsor. A few items to note in the request.

- Letter from OGCA to the agency/sponsor citing the amount of unobligated funds to be carried over and scientific justification of request

- The unit/department administrator should exercise due diligence to assure that the amount of carryover cited in the letter is less than or equal to the unobligated balance reported on the Financial Status Report (FSR)

- Plan for use of funds and budget (if required by the agency/sponsor)

Request to Lift a Restriction

Request sent to OGCA using the Award Request (AwaRe) Form. The process is facilitated by OGCA to the agency/sponsor. A few items to note in the request.

- Letter from OGCA to the agency/sponsor Letter to the agency/sponsor indicating how issues resulting in a restriction have been resolved

- Compliance/Protocol Approval Letters (as applicable)

- Fellowship Activation and Termination Notices - Activation or termination notices with signatures, as appropriate

Rules for Changing Salary Charges or Effort Commitments

The Federal government defines a significant change in work activity as:

- A 25 percent (or greater) reduction in the level of committed effort, or

- An absence from the project of three months or more, or

- A withdrawal from the project

The rules for changing salary charges and effort commitments depend on your project role and the nature and magnitude of the change.

For an investigator or key person:

If you want to: |

Then you must: |

| Reduce the salary charges without changing the effort commitment | Document as cost sharing the effort for which the sponsor will not provide salary support |

| Reduce both the salary charges and the effort commitment by less than 25% of the original commitment level | Document the change to the commitment level |

| Reduce both the salary charges and the effort commitment for a key person as listed in the NOGA by 25% or more of the original commitment level | Obtain approval from the sponsor prior to the change and in writing, and document the change to the commitment level when approved* |

| Reduce both the salary charges and the effort commitment for a key person listed in the proposal but not in the NOGA by 25% or more of the original commitment level | Document the change to the commitment level |

*For NIH awards, if the reduction in level of effort is addressed in the RPPR, a separate prior approval letter does not need to be sent to the NIH.

For a project staff member who is not an investigator or key person:

If you want to: |

Then you must: |

|

Reduce the salary charges without changing the effort |

Document as cost sharing the effort for which the sponsor will not provide salary support |

|

Reduce the salary charges and the effort by commensurate amounts |

No documentation, notification, or approval is required |

In the tables above, "NOGA" stands for Notice of Grant Award.

For a significant change in work activity, documenting the change means communicating it to OGCA after getting the sponsor's approval. For all other changes, documenting means maintaining a written or emailed record at the department/unit level.

Unallowable Costs

All costs proposed or incurred on a sponsored project must comply with the terms and conditions of the sponsored award in determining costs that are allowable or unallowable. At no time should unallowable costs be charged to a sponsored project.

Per Section 200.403 of Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, except where otherwise authorized by statute, costs must meet the following general criteria in order to be allowable under Federal awards:

- Be necessary and reasonable for the performance of the Federal award and be allocable thereto under these principles.

- Conform to any limitations or exclusions set forth in these principles or in the Federal award as to types or amount of cost items.

- Be consistent with policies and procedures that apply uniformly to both federally-financed and other activities of the non-Federal entity.

- Be accorded consistent treatment. A cost may not be assigned to a Federal award as a direct cost if any other cost incurred for the same purpose in like circumstances has been allocated to the Federal award as an indirect cost.

- Be determined in accordance with generally accepted accounting principles (GAAP), except, for state and local governments and Indian tribes only, as otherwise provided for in this part.

- Not be included as a cost or used to meet cost sharing or matching requirements of any other federally-financed program in either the current or a prior period. See also §200.306 Cost sharing or matching paragraph (b).

- Be adequately documented. See also §§200.300 Statutory and national policy requirements through 200.309 Period of performance.

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards

Verification of Charges (VOC) - Purpose

What is a Verification of Charges form?

A VOC form is used by OGCA as a communication tool with departments regarding various accounting questions. Some examples are:

- Unallowable charges

- This is where a charge has been made that is not allowed to be applied against that

particular award, typically because it was not budgeted for.

- To remedy, this will have to be removed to the departments Fund 1 account.

- Wrong account code

- This is where a charge has been coded incorrectly to a code that is not allowed to

be applied to the award.

- To remedy simply move the charge to an appropriate code.

- Overrun accounts

- This is when more has been spent on a fund than is budgeted for. Typically, we address overrun at the end of an awards life.

- This is where a charge has been coded incorrectly to a code that is not allowed to

be applied to the award.

- This is where a charge has been made that is not allowed to be applied against that

particular award, typically because it was not budgeted for.

What if I don’t agree that this is an unallowable charge or a wrong account code?

This is a communication tool meaning both parties can communicate their concerns. On the form there is a space for the department to put their justification/explanation. Simply fill out the form explaining how the charge(s) is appropriate and return it to the analyst.

- If further discussion is needed at this point the analyst will contact you directly to find a solution.

Why does OGCA use VOC forms?

One of the responsibilities of OGCA is to ensure that we are within compliance of award terms and conditions at all times. OGCA acts as a second set of eyes to double check that spending is allowable and being documented according to rules and regulations. Ultimately, we are attempting to protect the department and all members associated with the award from audit issues and any surprises occurring where money was improperly spent and demanded back by an agency.

What is the process for using VOC forms?

OGCA uses a three-step process for dealing with “problem” charges. Please note that the same VOC form is used for all three stages. The subject line of the email with the VOC form will always indicate if it is our 1st, 2nd, or 3rd attempt at communicating about the same charges.

- OGCA will send the VOC form to the department outlining the charges in question and request it back with an explanation of the resolution within 48 hours. If the VOC form is returned with a satisfactory justification for the charges or with an explanation of an action taken (eg. JV processed) then the issue is considered resolved and no further action will be taken.

- If the VOC is not returned within 48 hours, the same VOC will be sent again. This time the subject line of the email will indicate that it is your 2nd notification and the form itself will also state that it is your 2nd Again, if the VOC form is returned with a satisfactory justification for the charges or with an explanation of an action taken (eg. JV processed) then the issue is considered resolved and no further action will be taken.

- If the VOC form is not returned after the second notification, OGCA will send the

same VOC form for the 3rd This time the subject line will indicate that it is your 3rd notification, the form itself will indicate that it is your 3rd notification and the bottom of the form will be signed by the OGCA Analyst to notify

the department that if the form is not returned within 48 hours the charges will be

written off to their Fund 1. There are now two possible outcomes:

- If the VOC form is returned with a satisfactory justification for the charges or with an explanation of an action taken (eg. JV processed) then the issue is considered resolved and no further action will be taken.

- If the VOC form is not returned within 48 hours after the 3rd attempt, the charges will be removed from the award and charged to the departments Fund 1 account.